The ‘Gujarat model’ was the current BJP government’s defining selling point at the Centre stage in 2014, besides the Congress’ obvious mishaps, which won them the Lok Sabha election. Following through on various development projects, and angst against the “grand old party” is also what kept them in power in 2019 despite increased reports of lynching. But has there been inexcusable, preferential treatment towards the state? And if yes, at what cost?

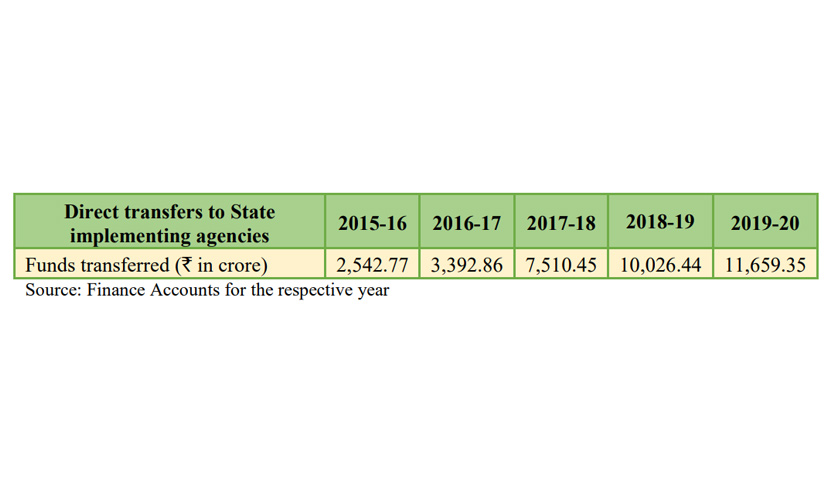

On the second day of the two-day Monsoon Session of the Gujarat Legislative Assembly last Tuesday, on September 28, the Comptroller and Auditor General of India (CAG) tabled the latest audit report on the assembly floor. The ‘State Finances Audit Report of the Comptroller and Auditor General of India’ for April 2019-March 2020 was the first audit report to be released for Gujarat this year. Following its public release, the report has invited scrutiny on the BJP government at the Centre, especially for the volume of direct transfers to Gujarat. According to the CAG, there was an increase of 350 percent in direct transfers, with Rs 11,659.35 crores sent to “state government implementing agencies” from the central government during 2019-20, as compared to Rs 2542.77 crores in 2015-16.

This is worrisome since transfers to such agencies are the prerogative of the state government depending on the funds available to it and priority. “With effect from April 1, 2014, Government of India decided to release all assistance for centrally sponsored schemes and additional central assistance to the state governments. In Gujarat, however, transfer of central funds directly to state implementing agencies continued even during 2019-20,” noted the CAG in the Gujarat assembly. Not only have the transfers continued, but the amounts have also increased leaps and bounds.

Problematic Findings

While Gujarat did not meet its projected tax revenue during 2019-20, it still reported a revenue surplus. However, the CAG has highlighted misreporting of the same. “In order to present better picture of State Finances, there is a tendency to classify revenue expenditure as capital expenditure and to conduct off budget fiscal operations,” notes the report after an audit of the deficits. Regardless, the revenue surplus relative to the gross domestic product (GSDP) stood at 0.12, the lowest in five years. The report says that there was an overstatement of Rs 1,886.39 crores for revenue surplus in 2019-20 by the state.

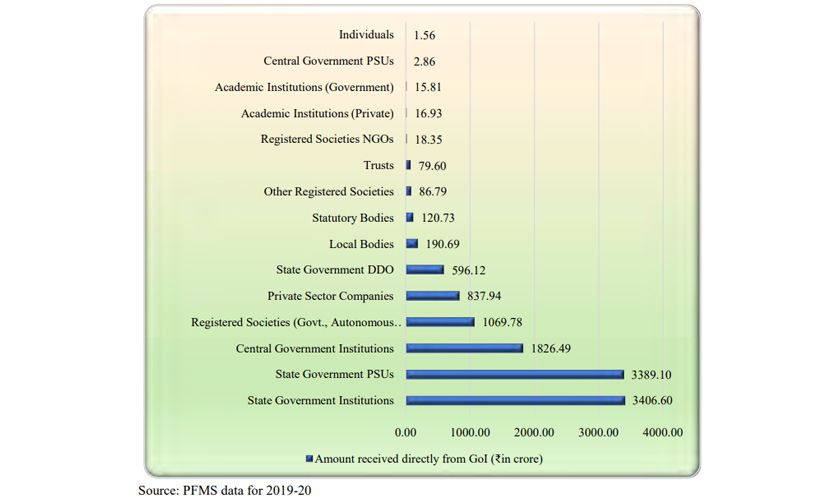

The CAG has also raised the need for more transparency after an audit of the public debt. Public debt also includes public-private partnerships that can be identified as contingent liabilities when “demand or other guarantees have been or are poised to be triggered”. Although the “state government implementing agencies” received the bulk of the funds i.e., Rs 7,772.35 crores, private sector companies in Gujarat also received a substantial amount of Rs 837.94 crores from the Government of India. In addition to this, Rs 86.79 crores were released to “other registered societies”, while Rs 79.60 crores were sent to trusts. In 2017, economist Indira Hirway had observed, “After huge incentives to corporate units, the Gujarat government is left with limited funds for education, health, environment and employment for the masses.” According to the audit report, “other than state implementing agencies” received a total of Rs 3887 crores.

The funds earmarked for the state have not been sent through the state budget. “Thus, to that extent, the state’s receipts and expenditure as well as other fiscal variables and parameters derived from them, did not present the complete picture,” notes the CAG report. It was also found that the accounts neither presented the receipts, nor reflected the flow of funds for 14,273 gram panchayats, which includes their opening balances and disbursements.

A total of 171 cases of misappropriation, losses, defalcation had been filed by the state government. The CAG’s report also points out the state administration’s inefficiency and “deficient monitoring mechanism”. The alleged land scam and corruption by the former chief minister of Gujarat, Anandiben Patel, the questionable decisions by the recently dropped former CM of the state, Vijay Rupani, along with the misreported and free flow of funds, have most definitely also been a contributor to the lack of health infrastructure that led to a significant number of deaths in Gujarat during the second wave of COVID-19.

Ambiguous Spending And COVID Mismanagement

Vijay Rupani, the former CM of Gujarat was asked to resign last month, before the completion of his five-year term. While there was a persistent disappointment with him and his inaction, Rupani’s decision to make the 108-ambulance compulsory for COVID-19 admissions was the final nail in the metaphorical coffin that buried his political career. According to the state government’s statement in the assembly last week, Gujarat received Rs 304.16 crores from the Centre for COVID management and treatment. Rupani and his cabinet’s removal from office, merely two weeks before the audit report was tabled in the assembly has also raised concerns.

The report concluded, “Indiscriminate operation of omnibus Minor Head 800 – Other Expenditure affected transparency in financial reporting and obscured proper analysis of allocative priorities and quality of expenditure.” The minor head in this scenario has not been defined under a major head. Therefore, the expenditure under this head in concerning. A similar instance was seen in Madhya Pradesh (MP), where an amount of Rs 34,831.64 crores was marked for “other receipts” under the omnibus Minor Head 800, and Rs 30,676.59 crores for “other expenditure” in 2018-19. However, despite being a state with a substantially lower population than Gujarat and MP, the Congress administered state of Chhattisgarh also saw an expenditure of Rs 3,447.19 crores as per “other receipts” under the minor head. Nevertheless, the report had no mention of direct transfers from the Centre.

Rajasthan, Karnataka and Tamil Nadu have similar population numbers as per the last census and have therefore, been taken up for comparison. Keeping in line with Gujarat, Rajasthan registered a direct transfer of Rs 9,483.87 crores from the Centre in 2019-20. Although in contrast, the Rajasthan state government reported 796 cases of misappropriation, theft, and loss across various departments, amounting to Rs 118.86 crores of government money. While the audit report for Karnataka did not mention any record of direct transfer of funds from the Centre, the report for Tamil Nadu has not been tabled. The CAG has recommended that the state of Gujarat needs to set “realistic budgets based on reliable assumptions of the needs”. Without outlining a budget provision, the state’s expenditure is in violation of financial regulations.

Limited Powers

The CAG’s reports are supposed to be taken cognisance of by the Public Accounts Committee (PAC). The committee consists of 22 members, 15 belonging to the Lok Sabha and 7 to the Rajya Sabha, who are appointed for a one-year term. It is headed by a member of the Opposition, who is appointed by the Lok Sabha speaker. The current head of the committee is Adhir Ranjan Chowdhury. The CAG’s findings are reviewed by the legislative assembly and the PAC. The committee requires the respective authorities to clear any discrepancies highlighted by the CAG. However, according to an official source, the committee reaches a final conclusion at least five years after the report is published. In Gujarat’s audit report for 2019-20, the CAG mentions, “Though the Audit Reports of the C&AG on State Finances are being prepared from the year 2008-09 onwards and presented to the State Legislature, these have not been taken up by the Public Accounts Committee for discussion.” Another official source also mentioned the tedium of analysing the audit reports, citing it as one of the reasons for the lack of follow ups and accountability.

The CAG does not have prosecution powers. He can investigate and audit an institution or body that he feels necessary to if a “substantial amount” has been released to it, with permission from the President of India, or the governor or administrator of the respective state or union territory. However, he cannot bring any charges and no action can be taken without a judicial probe. While the reports are all-encompassing and critical, their practical benefit seems unclear due to the limited powers awarded to the CAG. Recently, a division Bench comprising Justice U.U. Lalit and Justice Indira Banerjee also held that without statutory adjudication, a CAG report could not be the basis for recovery of cess.

Even though the reports may be of esteemed importance, their significance seems to diminish with such developments.

The Horus Eye is a weekly column written by Divya Bhan analysing current affairs and policies. This column does not intend or aim to promote any ideology and does not reflect the official position of The Sparrow.

Also read: Caste Politics – The Bane Of India’s Prowess

Also read: Farmers’ Protest: Justified Or An Unnecessary Impasse?